The development community has for years been heralding

microcredit as a means to escape poverty, but some very

simple math suggests that we need to be cautious about

pushing it too much.

To do this simple math, let�s compare the life-stories of

two fictional boys who are both born poor. Let�s call them

Micky and Savvy. Both work part time from age 10 earning 1

dollar per day, but they live at home with their parents,

who provide for their basic needs. Micky spends his hard

earned 7 dollars every week-end with his friends, while

Savvy saves them and manages to invest his modest funds at

an average real rate of return of 10% per year (mostly by

lending money to needy friends and relatives).

By the age of 20, they both move away from home and start

working full-time. Paid work only pays a miserable 3 dollars

per day, so Micky decides to start his own business instead.

He borrows 6500 dollars from a microfinance institution in

order to buy the necessary equipment to run his business (for

example a used car to become a taxi driver), and this allows

him to earn twice as much as a paid worker for the next 10

years (i.e. 6 dollars per day instead of 3, from age 20 to

age 30). The real interest rate charged by the microfinance

institution is 30% per year, so Micky wisely decides to

spend as little money as possible on himself (2 dollars per

day, which is right at the poverty line) and uses the

remaining 4 dollars per day to pay back his loan.

In contrast, Savvy does not have access to credit, so he has

to accept the job that pays the miserable 3 dollars per day.

Like Micky, he keeps his expenses low at 2 dollars per day,

which leaves 1 dollar per day in savings, which he manages

to invest at 10% per year, just as he has been doing since

he was 10 years old.

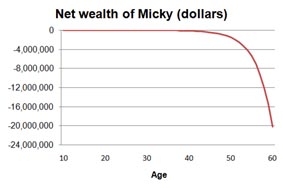

By the age of 30, Micky has handed over all his savings

during 10 years to the microfinance institution (14,600

dollars � more than twice the amount he borrowed and 2/3 of

everything he earned), but his debt has only grown, now

amounting to about 8,700 dollars. His equipment has worn out,

so he can no longer earn 6 dollars per day, and instead has

to take a regular job paying 3 dollars per day. He is now

heavily indebted, and has to reduce his expenditures to an

absolute minimum (1 dollar per day, which is at the extreme

poverty line). The remaining 2 dollars per day he pays to

the microfinance institution.

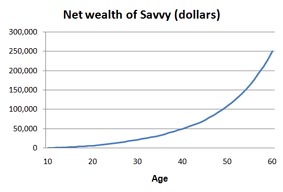

In contrast, Savvy has been building up his savings one

dollar per day, and by the age of 30 he is worth more than

20,000 dollars, so he decides it is time to improve his

living standards (he doubles his daily expenditures from 2

to 4 dollars). He is still only earning 3 dollars per day as

a regular, unskilled worker, but the returns on his small

investments allow the additional expenditure without

reducing his capital.

Unless Micky declares bankruptcy or otherwise defaults on

his debt, his debt will accumulate for the rest of his life,

reaching a staggering 20 million dollars by retirement age

(60 years). In contrast, Savvy can keep increasing his

expenditures regularly, reaching levels far above the

poverty level and far above his income level; and still see

his net wealth increasing. Figure 1 compares the net wealth

of Micky and Savvy over time under the abovementioned

assumptions.

Figure 1: Net wealth of Micky and Savvy, from age 10 to age

60

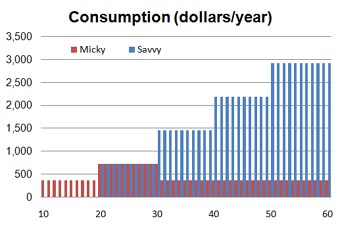

Figure 2 compares the annual consumption of Micky and Savvy.

Micky, due to his microcredit loan, has been living in

extreme poverty most of his life, with an accumulated

expenditure of only 23 thousand dollars during the 50 years.

Savvy, although he has earned only 48 thousand dollars in

accumulated labor income, was able to sustain accumulated

consumption of 76 thousand dollars and still has savings

worth a quarter of a million dollars.

Figure 2: Annual consumption of Micky and Savvy, from age 10

to age 60

A lousy little loan, which seemed like a good idea at the

time, doomed Micky to a life in extreme poverty and heavy

indebtedness, while Savvy, who couldn�t get a loan, did very

well. When real interest rates are above a few percent, it

makes a huge difference whether you are on the borrowing

side or the lending side of the credit transaction. And in

the world of poor people and microcredits, real interest

rates are always in the two digit range.

In some cases it makes sense to borrow money, even at 30%

interest. For example, if you borrow money to buy goods that

you are sure to sell very quickly, this may allow you to

take advantage of business opportunities that you would

otherwise be excluded from. This is why most micro credit is

used by the informal commerce sector. For productive

activities, microcredit rarely makes sense, and for housing

and consumption purposes it is a distinctly bad idea.

Microfinance institutions will of course never let debt grow

into the millions. Instead they would confiscate the few

assets the borrower has, including even his home. In case of

group credit, they may also confiscate assets from other

borrowers in the group, if these are unable to pay the debt.

The devastating consequences of not complying with the

monthly payments to a microcredit institution make defaults

relatively rare, as borrowers will do anything in their

power to comply, even borrowing informally at an even higher

rate.