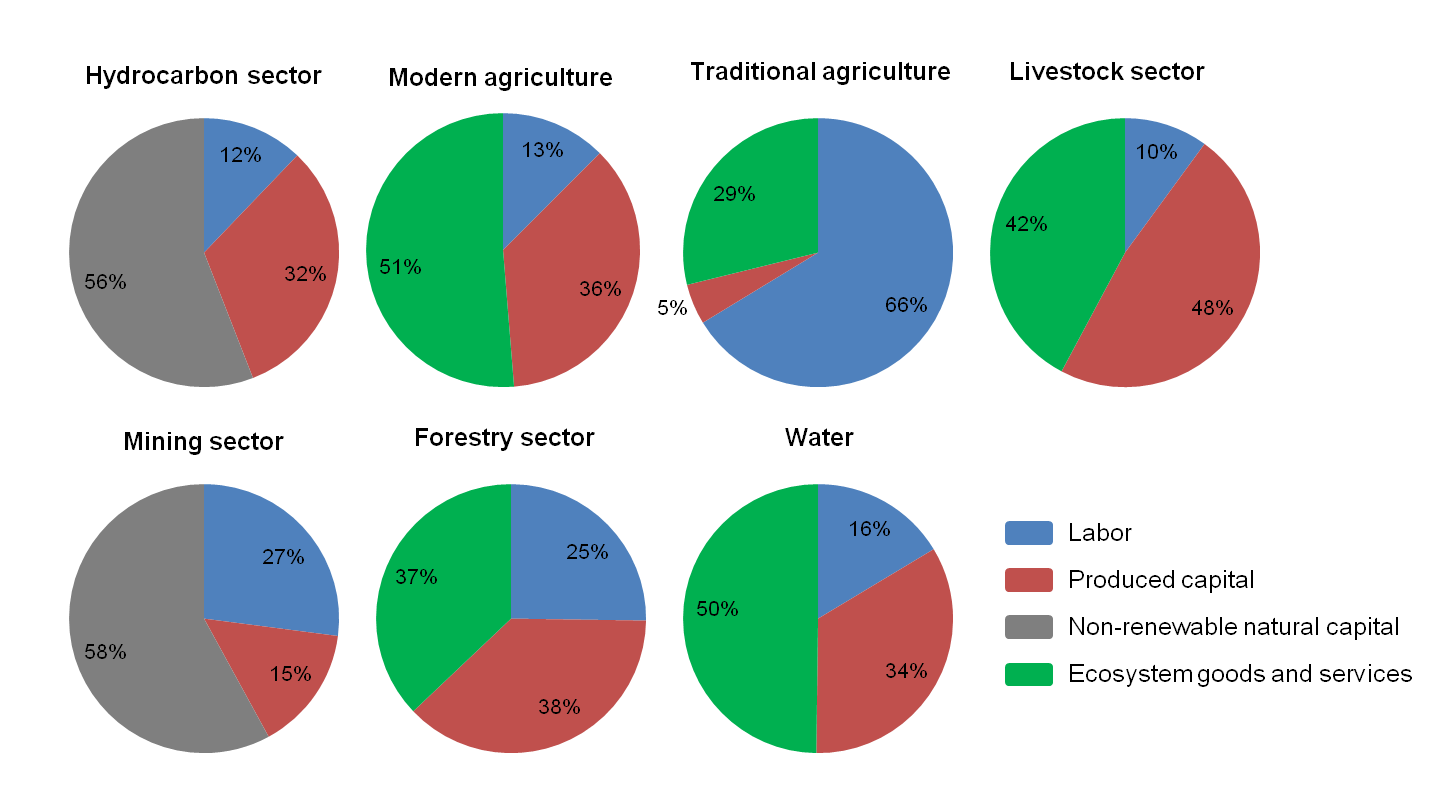

Green National Accounting (1) corrects one of the flaws

in conventional national accounting, which is ignoring

the important role of nature as a source of inputs into

production processes.

In some sectors these environmental inputs are very

important (e.g. forestry, farming and fishing), while in

other sectors they play a minimal role (e.g. banking,

commerce and education). In each sector they interact

with the two other conventional production factors,

labor and capital, to produce the total GDP for the

sector, but the proportions are different for each

sector (see Figure 1 for the sectors with a significant

environmental component):

Figure 1: The relative contribution of different factors

of production to sector GDP, Bolivia 2008

Source: Authors

elaboration based on (2).

The contribution of non-renewable natural capital and

ecosystem services (the grey and green slices) are

called natural resource rents. The benefits from these

rents should theoretically go to the owner of the

corresponding productive asset, which according to the

Bolivian Constitution would be the State. The State

should try to recover these rents in the form of

royalties or taxes, because otherwise producers would

capture these rents in addition to the normal, fair

payments for the labor and capital they have

contributed.

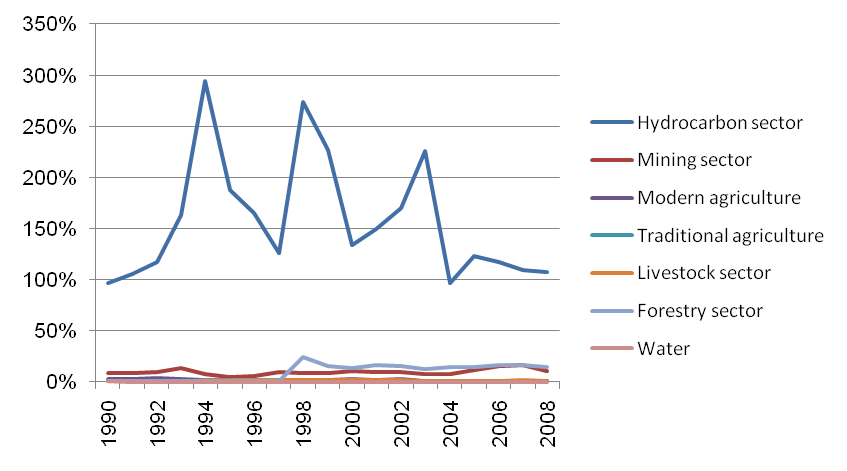

The Green National Accounts allow us to judge whether

the State manages to recover the resource rents in the

form of royalties or taxes in each sector. Figure 2

shows the percentage of natural resource rents which is

paid in producer taxes in each sector between 1990 and

2008. The aim should be to recover close to 100% of the

natural resource rents in each sector, but the figure

shows that this is only accomplished in the hydrocarbon

sector. Indeed, in most years, the State manages to

capture considerably more than 100% of the natural

resource rents in the hydrocarbon sector, suggesting

that the production companies (state and private) are

not getting fairly compensated for the labor and capital

invested. This could affect long-term sustainability of

the hydrocarbon sector, as the affected companies will

be reluctant to make the necessary investments.

Since 2004, the recovery of resource rents in the

hydrocarbon sector has been quite close to the target of

100% and the percentage has been relatively stable

compared to previous periods with wild fluctuations.

Figure 2: Producer taxes as percent of natural resource

rents in each sector, 1990 - 2008

Source: